Launching a software development startup in 2024 is challenging but exciting. The constantly evolving entrepreneurial landscape requires staying informed and prepared, especially in North America, a leader in global startup ecosystems. In 2023’s third quarter, this region invested about $31.4 billion in startup development, significantly focusing on software innovation.

This guide provides essential advice and insights for tech entrepreneurs, offering 10 key tips to navigate software development for the startup world. It’s designed to equip budding and experienced innovators with the knowledge needed for success in 2024’s dynamic business environment.

1

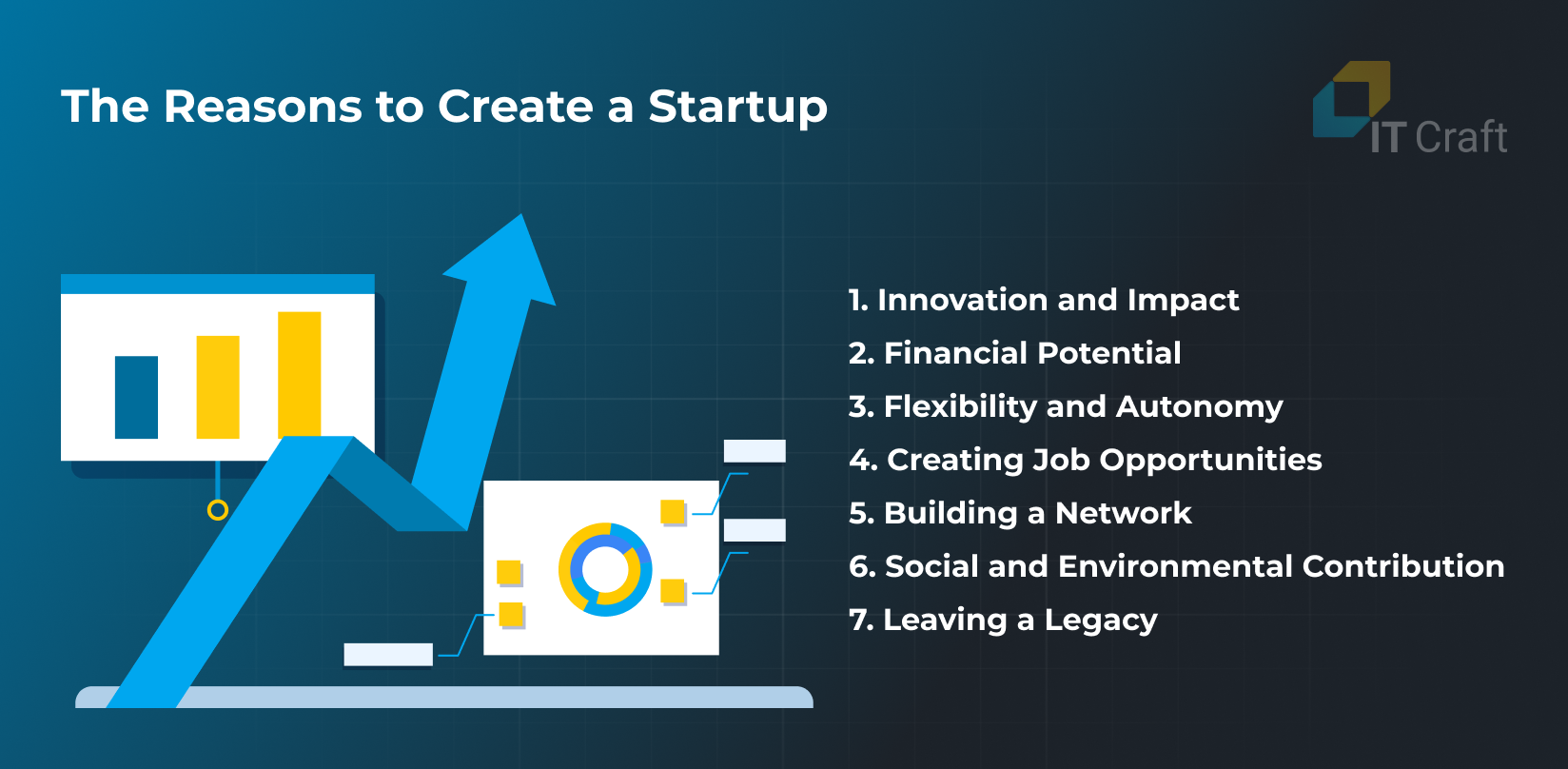

The Reasons to Сreate a Startup

Launching a startup from scratch can be one of an individual’s most challenging yet rewarding endeavors. While the path is often fraught with uncertainties and risks, its potential rewards and personal satisfaction are unparalleled.

Here are some compelling reasons to consider leaping into the world of startups:

- Innovation and Impact: Startups are often the birthplace of innovative ideas and groundbreaking technologies. Launching a startup business can bring your unique vision to life and potentially impact industries, communities, or the world. Discover powerful software startup ideas that can help you make a lasting impact.

- Financial Potential: Although starting a business comes with financial risks, the potential rewards can be substantial. Successful startups can yield significant financial returns for founders, early employees, and investors.

- Flexibility and Autonomy: Running your startup means having the freedom to set and work towards your goals. This level of autonomy and flexibility is rarely found in traditional employment settings, allowing for a more personalized and fulfilling work experience.

- Creating Job Opportunities: As your startup grows, so does your team. You can create jobs and cultivate a workplace culture that aligns with your values. This can be incredibly rewarding as you contribute to the economy while building a supportive and motivated team.

- Building a Network: Entrepreneurs inevitably build a broad network of contacts, including other entrepreneurs, investors, customers, and advisors. These connections can be invaluable resources for advice, mentorship, and future opportunities.

- Social and Environmental Contribution: Many startups are founded to address social or environmental issues. If you are motivated to make a difference, a startup can be an effective platform for enacting positive change.

- Leaving a Legacy: Building a successful startup can be part of your legacy, a testament to your hard work, innovation, and determination. It’s an opportunity to create something lasting and impactful.

Ready to innovate and lead?

Unlock your creative potential, revolutionize industry practices, and carve out tomorrow's landscape with innovation.

Join Us

2

10 Tips for Making a Successful Startup

Creating a successful startup involves innovation, perseverance, and strategic planning. Here are ten comprehensive tips that encompass various aspects of building a successful startup:

Validate Your Idea

As 71% of IT projects experience deadline delays, choosing discovery phase services can place you among the successful 29% that stay on schedule.

Before taking the plunge, ensuring that your startup idea is viable and has a demand in the market is critical.

- Market Research: Confirming your startup idea’s feasibility and market demand is vital. Undertake comprehensive market research to understand industry trends, customer needs, and the competitive landscape.This involves conducting thorough market research to understand industry trends, customer needs, and the competitive landscape.

- Customer Engagement: Engage with potential customers through surveys or focus groups. This provides valuable insights into their preferences and challenges. Engaging with potential customers through surveys or focus groups can provide valuable insights into their preferences and pain points.

- Early Validation: Validating your concept early can save you valuable time and resources and guide your product development in the right direction.Validating your concept early on can save you valuable time and resources and guide your product development in the right direction.

Develop a Solid Business Plan

A solid business plan is the foundation of a successful startup. It should encompass the following:

- Business Model Clarity: Detail your business model, including your operational strategy, revenue generation methods, and sustainability plans. This clarity will help in communicating your vision to stakeholders and team members.

- Market Analysis: Provide an in-depth analysis of your target market. Understanding your audience, behaviors, and preferences is key to effectively tailoring your product and marketing strategies.

- Marketing Strategies: Outline your strategies for reaching your target market. This includes a mix of digital and traditional marketing tactics, ensuring a comprehensive approach to customer acquisition and engagement.

- Financial Projections: Include detailed financial projections and long-term goals. This aspect is crucial not just for internal planning but also for attracting investors and securing funding.

Focus on Building a Strong Team

The team behind a startup is as important as the idea itself. Focus on:

- Skillful Recruitment: Find individuals who are not only skilled but who also share your vision and passion for the venture. The right team members can drive your startup toward success and help you overcome various challenges.

- Diversity and Innovation: Encourage diversity in skills and perspectives within your team. This diversity fosters innovation creativity, and can lead to more effective problem-solving strategies.

- Positive Team Culture: Cultivate a culture that encourages collaboration and open communication. A positive and supportive environment is essential for team morale and productivity, which in turn contributes to the startup’s overall success.

Embrace Lean Startup Principles

Integrating lean startup principles into your business strategy can significantly streamline your path to success. This approach emphasizes efficiency and adaptability:

- Minimum Viable Product (MVP): Start by developing a minimum viable product, a foundational version of your product with just enough features to satisfy early adopters. The MVP is a strategic tool to test your idea in the market using minimal resources, reducing initial investment and risk.

- Iterative Development: The feedback on your MVP is invaluable. Use it to make iterative improvements to your product. This process of continuous refinement ensures that the final product meets customer needs and preferences, greatly enhancing its market relevance and appeal.

Prioritize Customer Feedback

Customer feedback is a crucial element for any startup’s growth and refinement:

- Continuous Feedback Loop: Regularly seeking and prioritizing customer feedback is essential. This feedback serves as a rich source of information, revealing what aspects of your product or service resonate with your audience and what areas require enhancement.

- Building Customer Relationships: Beyond gathering insights, engaging with your customers helps build brand loyalty and a sense of community. By actively listening to your audience and incorporating their feedback, you improve your product and strengthen your customer relationship, turning them into brand ambassadors.

Effective Cash Flow Management

Effective financial management is crucial for the stability and growth of your startup. This is particularly true in the early stages, where resources are often limited:

- Cash Flow Monitoring: Keep a diligent eye on your cash flow. Regularly track and manage the money coming in and going out of your business. This vigilance is key to understanding your financial position at any given time.

- Cost Control: Be strategic in minimizing unnecessary expenses. Cutting down on non-essential spending can free up resources that can be better utilized in areas critical to your business growth.

- Smart Investments: Make informed investments. Each investment should be weighed for its potential return and contribution to your business’s sustainability and growth.

Build a Strong Brand and Online Presence

In today’s digital age, having a strong brand and online presence is indispensable:

- Brand Development: Create a compelling and visually appealing brand identity. Your brand should resonate with your target audience and reflect your startup’s core values and vision.

- Digital Marketing Strategy: Develop a comprehensive digital marketing strategy. This strategy should effectively reach and engage your target audience through various online channels.

- Online Engagement: Establish a robust online presence. This includes having a professionally designed website and being active on relevant social media platforms. A strong online presence enhances your visibility and bolsters your credibility in the market, making it easier to attract customers and partners.

Network and Seek Mentorship

The importance of networking in the entrepreneurial journey cannot be overstated. Building a strong network and seeking mentorship offers numerous benefits:

- Building Connections: Actively network with fellow entrepreneurs, industry experts, and potential mentors. These connections can lead to new opportunities, partnerships, and avenues for growth.

- Gaining Valuable Advice: Interacting with those in your industry provides access to a wealth of knowledge and experience. This can be crucial in making informed decisions and avoiding common pitfalls.

- Mentorship Benefits: Seek mentorship from experienced individuals in the startup ecosystem. Mentors offer guidance, support, and insights gained from their own experiences, which can be invaluable in navigating the complexities of the startup world.

Stay Agile and Adapt

In the dynamic startup environment, agility and adaptability are key to survival and success:

- Flexibility in Strategy: Be ready to adjust your business strategy in response to changing market conditions, technological advancements, and consumer trends. This flexibility allows you to stay relevant and competitive.

- Adapting to Feedback: Pay close attention to customer feedback and be willing to modify your product or services accordingly. This customer-centric approach ensures that you are always aligned with market needs.

- Seizing Opportunities: Staying agile enables you to capitalize on new opportunities quickly. Whether it’s a shift in consumer behavior or a new technological breakthrough, adaptable positions you to lead rather than follow in your industry.

Protect Your Intellectual Property

Securing your startup’s intellectual property (IP) is a critical aspect of ensuring its long-term success and maintaining a competitive advantage:

- Early IP Protection: Ensure you secure the appropriate protections for your intellectual property, such as patents, trademarks, or copyrights, as early as possible. This proactive approach can safeguard against future legal issues and intellectual property infringement.

- Comprehensive IP Strategy: Develop a comprehensive strategy for protecting your IP. This includes identifying all aspects of your business that can be protected and understanding the different types of IP protection available.

- Prevent Infringement: Implement measures to monitor and enforce your IP rights. This vigilance is essential in protecting your assets from unauthorized use or infringement, which could otherwise compromise your market position and profitability.

Embrace Technology for Operational Efficiency

Incorporating technology and tools into your business processes can greatly enhance efficiency and give your startup a competitive edge:

- Streamlining Operations: Utilize technology to streamline your business operations. This includes automating repetitive tasks, optimizing workflows, and improving communication channels within your team.

- Enhancing Productivity: Leverage tools that boost productivity. Project management software, analytics tools, and other digital resources can help manage projects more effectively and make data-driven decisions.

- Competitive Advantage through Technology: Embrace the latest technology trends relevant to your industry. Staying ahead in technological advancements can provide a significant competitive advantage, allowing you to innovate faster and serve your customers more effectively.

Understand Your Legal Obligations

Understanding and adhering to the legal aspects of running a startup is fundamental:

- Legal Compliance: Familiarize yourself with the legal requirements pertinent to your startup, including necessary registrations, licenses, and tax obligations. Compliance with these legalities is mandatory and vital in avoiding potential legal hurdles.

- Regulatory Landscape: Keep abreast of your industry’s changing legal and regulatory landscape. This proactive approach can help anticipate and adapt to legal changes, thereby maintaining uninterrupted business operations.

Strategize for Effective Scaling

Developing a well-thought-out strategy for scaling your business is crucial:

- Growth Management: Plan your scaling process by understanding the right timing for expansion and how to manage growth sustainably. This involves assessing market conditions, customer demand, and your business’s operational readiness for development.

- Resource Planning: Anticipate the resources needed for scaling, such as additional staffing, technology upgrades, and financial investment. Effective planning ensures you have the necessary infrastructure to support your business’s growth.

Focus on Sustainability

Making sustainability a central part of your business ethos is not just beneficial, it’s increasingly becoming a necessity:

- Holistic Success Metrics: Move beyond solely focusing on financial metrics. Acknowledge the significance of your startup’s environmental and social impact. By integrating sustainable practices, your business contributes positively to society and enhances its reputation.

- Eco-Conscious Operations: Actively implement strategies to minimize your environmental impact. This can range from utilizing renewable energy sources to adopting sustainable supply chain practices and eco-friendly materials.

Prepare for Challenges

Anticipating and preparing for potential challenges is essential in the ever-changing landscape of startup development:

- Embracing Resilience: Recognize that encountering setbacks is a natural part of the startup journey. Cultivating resilience, maintaining a persistent attitude, and fostering a positive outlook are crucial for overcoming these hurdles.

- Adaptive Problem-Solving: Encourage a culture of strategic problem-solving and flexibility within your team. Developing this adaptive approach ensures that your startup can quickly pivot in response to market changes, customer feedback, or unforeseen challenges.

Leveraging AI for Startup Innovation

Incorporating Artificial Intelligence (AI) into your startup can significantly enhance innovation and competitiveness. AI technologies allow startups to automate complex processes, gain insights from data analytics, personalize customer experiences, and innovate product offerings.

By strategically integrating AI, startups can optimize operations, make data-driven decisions, and create unique value propositions that stand out in the market. Embracing AI propels startups towards technological advancement and opens up new avenues for growth and scalability.

Following these tips and remaining committed to your vision can significantly increase your chances of building a thriving and sustainable business.

Eager to turn your vision into reality?

Unlock your entrepreneurial journey with battle-tested strategies, paving your path to resounding success.

Start Your Adventure

3

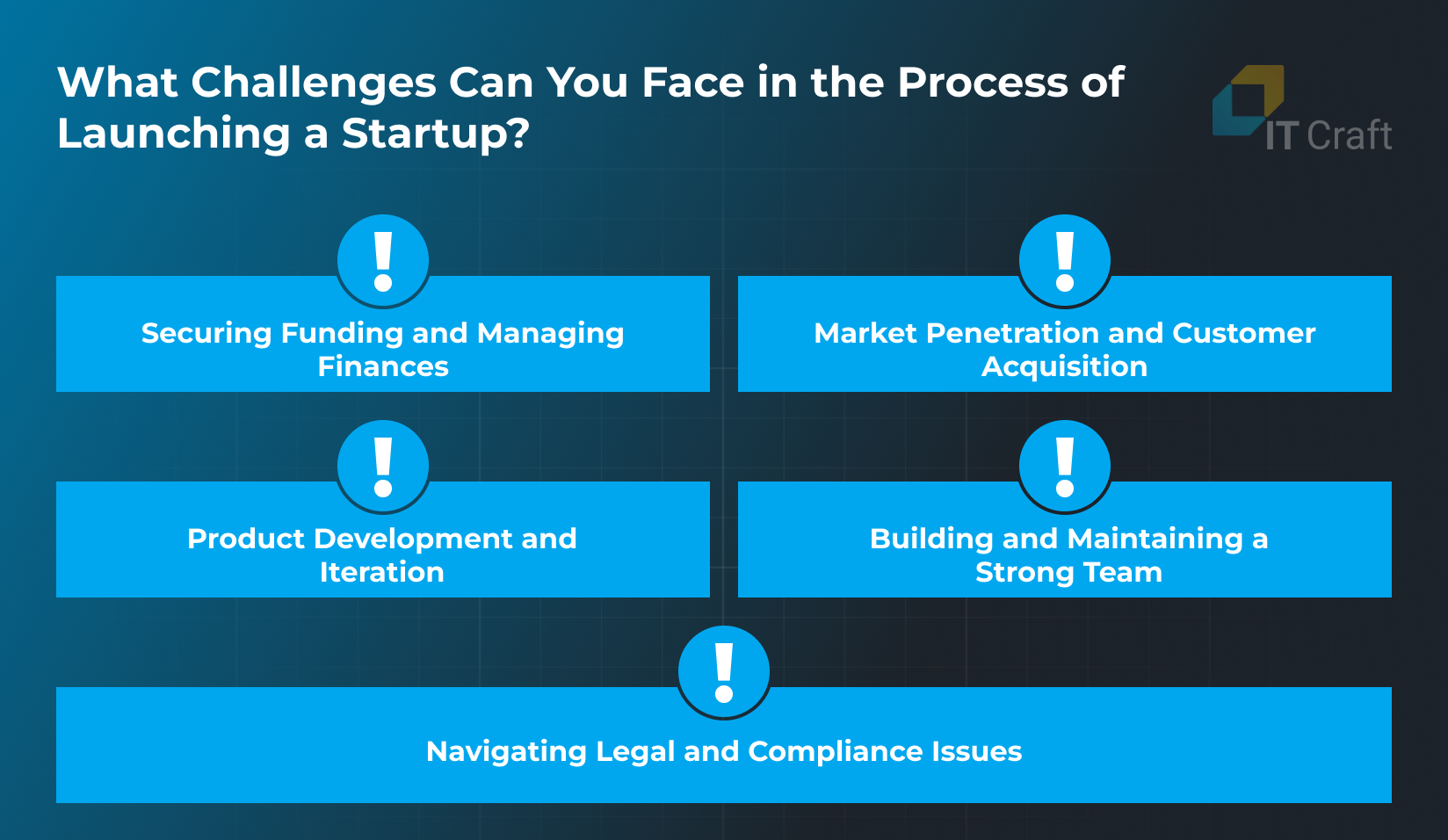

What Challenges Can You Face in the Process of Launching a Startup?

Starting a startup is akin to embarking on a thrilling yet challenging adventure, where each step can lead to discoveries and unforeseen hurdles. Entrepreneurs venturing into this dynamic terrain must be well-equipped to face many challenges that test their resolve, creativity, and strategic thinking.

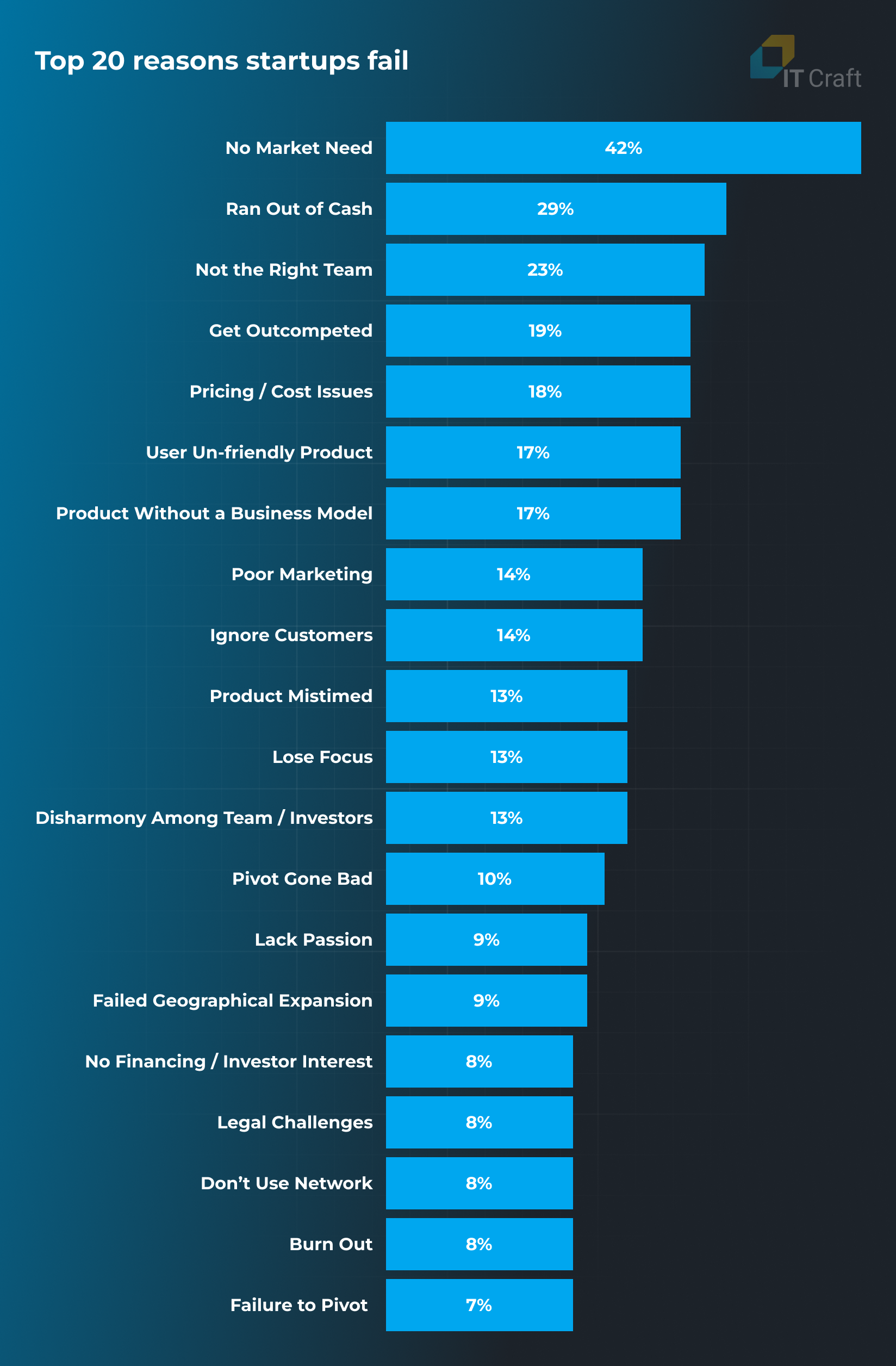

CB Insights cites the lack of market demand as the primary cause of startup failures, often stemming from unclear business objectives and an inability to fulfill user requirements.

Here’s a deeper dive into the common challenges you might encounter while launching a startup and how to navigate them effectively:

Product Development and Iteration

Developing a product that meets market needs and stands out in a crowded marketplace is a significant challenge. Startups must manage the delicate balance between innovation, functionality, and user-friendliness.

This involves the initial development phases and continuous iteration based on user feedback. Agile development methodologies can aid in this process, allowing for flexible and adaptive product development.

Regularly collecting and analyzing user feedback, whether through surveys, beta testing, or user analytics, is essential to refine and improve the product. The challenge also involves managing resource constraints and technical challenges while striving to deliver a product that meets market demands.

Building and Maintaining a Strong Team

The success of a startup often hinges on the strength of its team. Finding the right mix of skills, personalities, and work ethics can be challenging. It involves identifying individuals with the necessary technical skills and experience and those who share the startup’s vision and culture.

A brief stat on this point:

Once the team is assembled, the focus shifts to maintaining a healthy and productive work environment. This includes fostering open communication, encouraging collaboration, and managing conflicts.

Startups must also focus on retaining talent through competitive compensation, growth opportunities, and a positive work culture.

Securing Funding and Managing Finances

Securing funding is a key challenge for tech startups, requiring navigation through various sources like venture capital, angel investment, crowdfunding, and loans. Around 33% of startups initiate operations with less than $5,000, which falls significantly short of the necessary capital for success.

Each nuances with its expectations, such as equity stakes or repayment terms. Crafting an effective pitch and business plan that communicates your value proposition, market potential, and revenue model is crucial.

Once funding is secured, the challenge shifts to prudent financial management.

Startups must navigate cash flow management, budgeting, and financial planning to ensure sustainability and growth.

This includes making strategic decisions about expenses, investments, and resource allocation to maximize the impact of every dollar.

Market Penetration and Customer Acquisition

Gaining a foothold in the market, particularly with established players, requires more than a great product or service.

For example, McKinsey reported that the most significant hurdle for fintech startups is often the high expense associated with acquiring new customers.

Startups must grasp their target market’s behaviors and preferences, segment the market, and create resonant marketing strategies. Leveraging digital and social media marketing is key to raising brand awareness and attracting customers.

However, the challenge continues after acquisition; retaining customers through excellent service, continuous engagement, and adapting to their changing needs is equally crucial for long-term success.

Navigating Legal and Compliance Issues

Startups must navigate a complex web of legal and compliance issues ranging from business registration and tax compliance to employment laws and protecting intellectual property.

It has become increasingly common for founders and startups to encounter significant regulatory challenges. This is evident in various sectors, such as healthcare, where Zenefits’ CEO and Co-founder Conrad Parker had to step down and was later penalized with fines around $500K.

Understanding and adhering to these legal requirements is crucial to avoid potential legal pitfalls. This involves initial compliance and staying updated with changing regulations and laws.

Startups often require expert legal advice to navigate these waters, which can add to the operational costs but is essential for safeguarding the business.

By understanding these challenges in-depth and preparing for them, entrepreneurs can significantly increase their chances of building a successful and sustainable startup.

4

How to build a startup marketing plan?

Building a marketing plan for a startup is critical in establishing a strong presence in the market and attracting the right audience. A well-crafted marketing plan outlines how you will reach your potential customers and helps align your marketing efforts with your business goals.

Here’s how to create an effective marketing plan for your startup:

1 Understand Your Target Market & ICP:

- Market Research: Begin with thorough market research to understand your target audience’s needs, preferences, and behaviors.

- Customer Personas: Create detailed customer personas that represent your ideal customers. This will help in tailoring your marketing strategies to specific audience segments.

2 Define Your Unique Selling Proposition (USP):

- Identify What Sets You Apart: Determine what differentiates your product or service from competitors. Your USP should address a unique problem or offer a distinct benefit to your target audience.

- Communicate Your USP Clearly: Ensure that your USP is communicated in all your marketing materials and campaigns.

3 Set Clear Marketing Goals and Objectives:

- Align with Business Goals: Your marketing objectives should align with your overall business goals, whether it’s increasing brand awareness, generating leads, or driving sales.

- SMART Goals: Set Specific, Measurable, Achievable, Relevant, and Time-bound goals to ensure they are clear and actionable.

4 Choose the Right Marketing Channels:

- Identify Where Your Audience Is: Based on your target audience, choose the marketing channels that will be most effective. This could include social media, email marketing, content marketing, SEO, or paid advertising.

- Budget Considerations: Allocate your budget across these channels based on their effectiveness and your available resources.

5 Develop Your Content Strategy:

- Valuable and Relevant Content: Create content that provides value to your audience, whether it’s informative blog posts, engaging social media content, or compelling email newsletters.

- Content Calendar: Plan a content calendar to maintain a consistent posting schedule and cover various topics relevant to your audience.

6 Implement SEO Best Practices:

- Optimize for Search Engines: Implement SEO strategies to improve your website’s visibility in search engine results. This includes keyword research, on-page optimization, and building high-quality backlinks.

- Local SEO: If your startup targets a local audience, focus on local SEO strategies to attract customers in your area.

7 Leverage Social Media Marketing:

- Active Social Media Presence: Establish a strong presence on social media platforms where your audience is most active.

- Engagement: Focus on engaging with your audience through regular posts, responses to comments, and interactive content.

8 Leverage Social Proof

- Strategic Listings: Ensure your business is listed on relevant online directories and platforms that align with your industry and audience demographics.

- Gather Customer Testimonials: Actively seek feedback from satisfied customers and request permission to share their positive experiences on your website and social media.

- Showcase Reviews and Ratings: Prominently display customer feedback and ratings on your website and social media to prove your product’s quality and appeal to potential customers.

9 Track and Analyze Performance:

- Use Analytics Tools: Utilize tools like Google Analytics, social media analytics, and email marketing software to track the performance of your marketing efforts.

- Adjust Strategies Based on Data: Regularly review your performance data and adjust your marketing plan to improve results.

10 Continuously Iterate and Improve:

- Stay Adaptable: The market and customer preferences can change rapidly, so be prepared to adapt your marketing strategies accordingly.

- Feedback Loop: Collect feedback from customers and use it to refine your marketing approach and product offerings.

Remember, a marketing plan for a startup should be flexible and adaptable as the business grows and market conditions change. It’s a continuous learning process, experimenting and refining strategies to find what works best for your startup.

5

How Much Does It Cost to Start a Startup?

Understanding the average costs in your industry can provide a ballpark estimate of the expenses involved in starting a small business. As your business expands, managing payments and choosing cost-effective materials is crucial.

Minimizing costs can significantly enhance the return on investment from your business offerings. The specific expenses you’ll face will depend on various factors, including:

- The scale of your business operation.

- Whether your business is based in a physical location or operates online.

- The number of employees you plan to hire.

- The cost of the inventory you need to stock.

- Expenses related to producing goods, such as labor and raw materials.

When calculating your startup costs, paying attention to them is important. Expenses can increase as the business grows. Overlooking smaller costs in the early stages can lead to financial challenges later.

6

Our Experience in Launching Startups

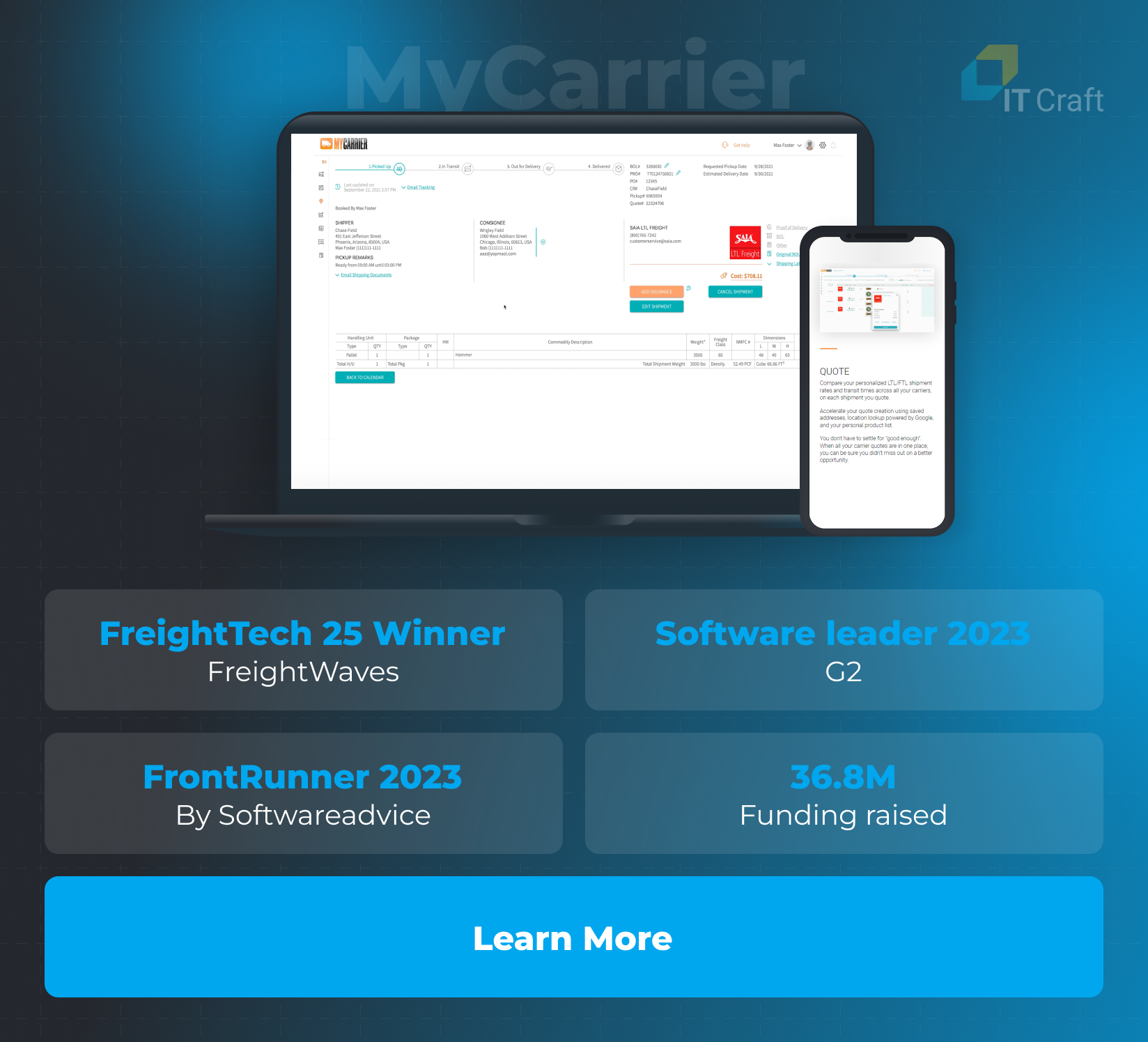

MyCarrierTMS: Revolutionizing Transportation Management

Since 2017, IT Craft has played a critical role in the evolution and success of MyCarrierTMS, a specialized portal for transportation management focusing on truckload shipments. This collaboration has led to significant milestones and growth in the logistics sector.

The partnership led to the creation of a comprehensive web solution from the ground up, effectively validating and elevating the business model of MyCarrierTMS. The operation experienced rapid growth, facilitating several funding rounds, a testament to the project’s success and potential.

Key Milestones:

- The project began with an MVP focused on less-than-truckload shipments, attracting an impressive $36.8M in funding.

- MyCarrierTMS was recognized in the industry, earning the FreightWaves FreightTech 25 Award and being named the top TMS software by G2, highlighting its impact and innovation in transportation management.

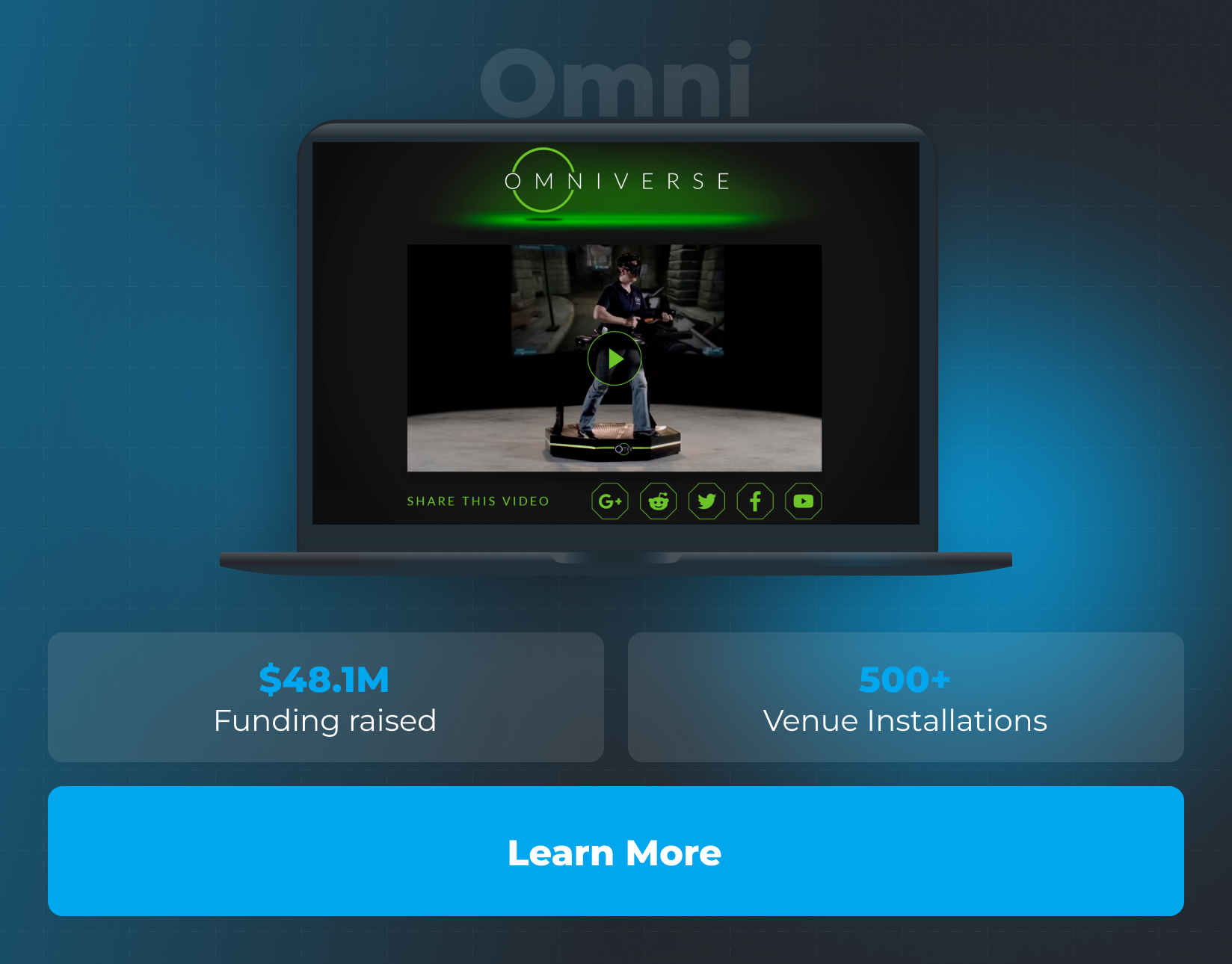

Omni: Leading Innovations in Virtual Reality

ITCraft’s expertise has also significantly contributed to Omni’s success in the virtual reality sports and gaming arena. A dedicated team of seven at ITCraft has been at the forefront of driving advancements in VR technology, influencing gaming, esports, and entertainment.

The Omni project’s achievements are substantial and widely recognized:

- Despite the compact design of the Omni Arena, it has become a popular feature in various venues, offering an optimal space-efficient yet appealing VR experience.

- The technological backbone of the Omni Arena includes sophisticated technologies like AngularJS, Unreal Engine, .NET 5, and .NET Core 2.1, ensuring a cutting-edge user experience.

Expansion and Global Reach:

- The project saw a major turning point with the successful launch of an MVP, which opened doors to a significant funding of $48.1M.

- Demonstrating its stable performance and appeal, the Omni product has been installed in over 500 venues across 45 countries, showcasing its global impact and scalability in the VR industry.

!

Conclusion

Launching a startup demands strategic foresight, adaptability, and resilience. The key takeaways from our guide highlight the importance of thorough planning, understanding market dynamics, and being prepared to adapt. Remember, the path to success in the startup world is as challenging as rewarding.

Stay committed to your vision, embrace the learning process, and seize the opportunities of the ever-evolving business landscape . With the right partner in software development for startups, your idea has every chance to grow into something truly impactful.